How do Insured Sweep Accounts work?

Suppose you have a customer with $1 million in deposits that is safety conscious. Using an Insured Sweep Account, you can provide the client with a single account that offers access to millions in aggregate insurance across network banks*.

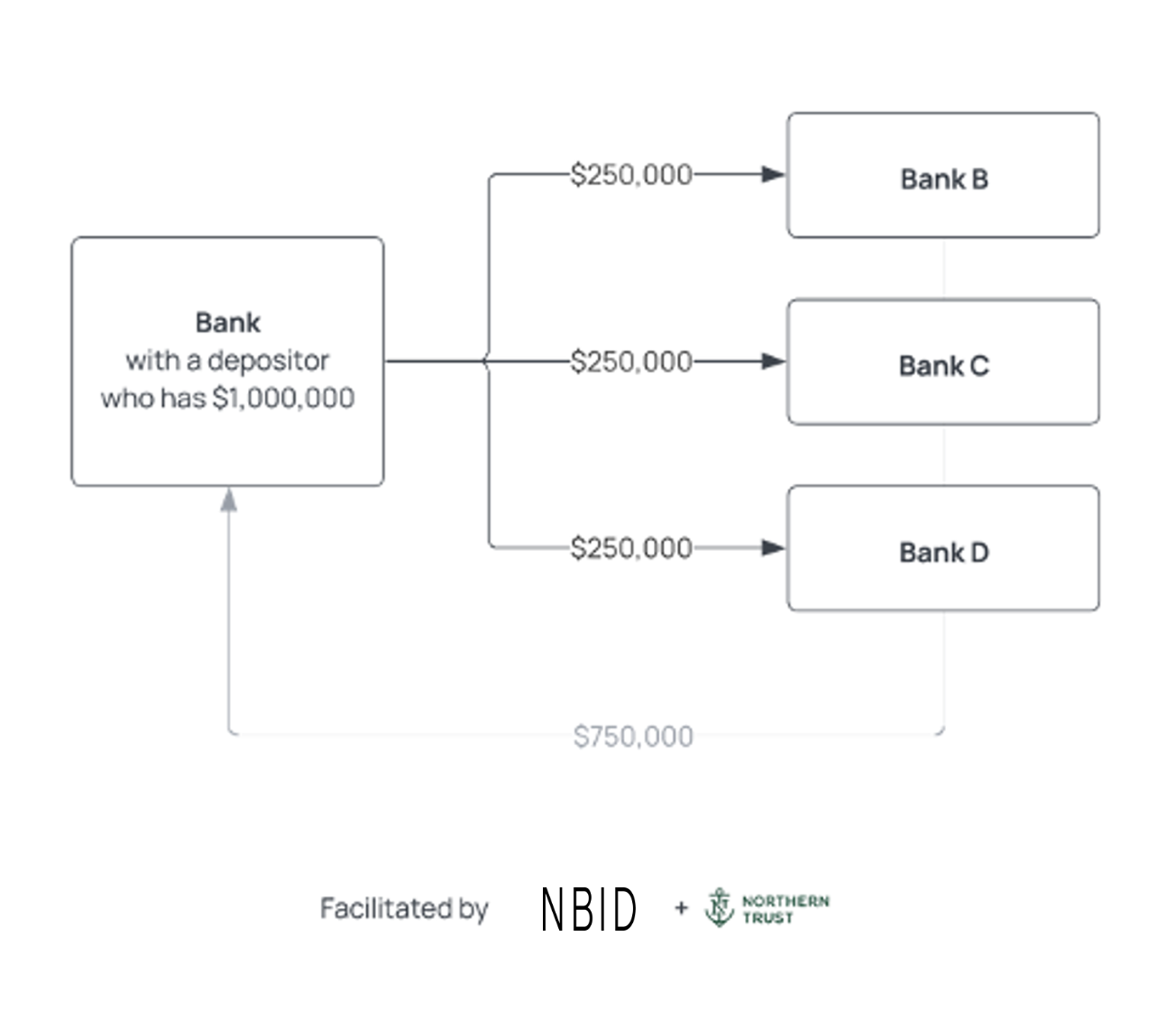

To make balances in the Insured Sweep Account eligible for insurance, funds are distributed to other banks in the NBID network in increments not exceeding the $250,000 Standard Maximum Deposit Insurance Amount. In this example, the first $250,000 will be allocated to one bank, another $250,000 to a second bank, an additional $250,000 to a third bank, and the remaining $250,000 can stay with your bank. By placing less than $250,000 at each bank, the entire account balance is eligible for insurance coverage (provided certain pass-through conditions are met).

Using Insured Sweep Accounts allows your bank to attract and retain large-value customers such as businesses, public funds, and higher-net-worth individuals. For your clients, it eliminates the need to keep track of multiple accounts at various banks. All transaction activity and network allocations are consolidated into one simple statement for clients.

*A list identifying NBID network banks can be found here. NBID is not FDIC-insured banks, and deposit insurance covers the failure of an insured bank. Certain conditions must be satisfied for “pass-through” FDIC deposit insurance coverage to apply.

Updated 3 months ago